During one-month period to 31st January, major equity markets, as measured by the aggregate

FTSE All – World Index rose marginally against a background of mixed Covid-19

developments and political change. Apart from Asia and Emerging Market equities,

most indices showed a broadly similar return, especially in sterling adjusted

terms. The VIX index rose to a

level of 31.9rising sharply near the month end during the retail/hedge fund

speculative “battle†(see below). Government stocks, on the other hand mostly fell

in price terms, the US 10 year for instance, breaching 1% for the first time

since March 2020.Currency moves were relatively muted, the pound strengthening

a little, while the Chinese Yuan showed further gains against the Dollar. Commodities

were generally firmer though gold, silver, coal, and iron ore slipped in price

terms.

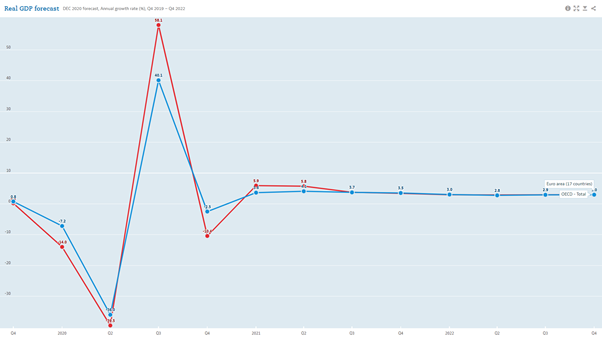

Recent US Federal reserve meetings have reiterated the adoption of the new monetary policy strategy that will be more tolerant of temporary rises in inflation, cementing expectations that the US central bank will keep interest rates at ultra-low levels for years, as well as maintaining bond purchases. This stance was reiterated in the January2021 Fed meeting. A combination of this, plus the debt-funded stimulus package (more handouts, economic and health spending) recently proposed by new President Joe Biden, worth about 9% of pre-crisis GDP, on top of earlier government help (approx. 3 trillion Dollars up to December 2020), is igniting the possible medium term “overheating debateâ€. Shorter term economic indicators point to a softening labour market, particularly in hospitality and travel and declining real consumer spending in November and December. Currently, reasonable vaccine news must be balanced against tighter anti Covid restrictions advocated by the new President. Provisional GDP data just released showed fourth quarter of 1% compared with the previous quarter, somewhat lower than estimates, producing an overall 2020 decline of 3.5%. Recently revised economic forecasts are now expecting over 5%-6% growth for 2020 with unemployment ticking down to around 4.5%.

At the ECB December meeting the emergency aid programme was increased, and the 1.8 Trillion Euro loan approved. The January meeting saw interest rates maintained at -0.5% and a continuance of the pandemic bond buying programme. Very recent European sentiment surveys pointed to weakening economies at the end of 2020, although in some cases, not as weak as expected, and lockdowns of varying intensity have been imposed to February and March and Easter in certain areas.

Not surprisingly the service sector is suffering more than manufacturing, the German manufacturing PMI, for example, rising over the same period, with exports to China being particularly strong. Countries with high tourism dependency are clearly suffering disproportionately. Political developments in Germany (new CDU leader), Holland (anti-curfew riots, social payment scandal) and Italy (Conte under more pressure) were not especially market sensitive.

Asia excluding Japan, led by China (across all sectors and property), remains in better shape than other major regions (virus response, economic mix). Korea for example expects a 2020 GDP decline of just 1.5%, while growth is expected in Vietnam and Taiwan (just reported +3.0% for 2020), the latter heavily dependent on the export of electrical components/devices. Japan, with a relatively muted Covid-19 experience, is expected to experience a relatively smooth transition under the new PM, Yoshihide Suga and experienced 5% growth in the third quarter, higher than expectations. However, inflation continues to disappoint with a price drop of 1% in December, Suga’s approval rating is dropping and any cancellation/deferral of the Olympics (July?), currently under discussion ,will not help investor sentiment.

China continues to report relatively strong economic data, showing 2020 full year economic growth of 2.3%, factory output far outstripping consumer spending. Forecasts of 5% to 6% are starting to emerge for 2021.In a surprise move a few days ago the People’s Bank of China withdrew $12 billion from the banking system, which although a relatively small amount followed recent statements concerning “overheating†in certain asset classes and is the first “tightening†move by any major economy. Any further moves, plus fallout from US sanctions (MSCI taking some stocks out of index) on top of last year’s gains may dampen equity enthusiasm going forward despite the relatively strong economic growth, and extra due diligence is warranted.

Within the UK, official GDP figures, showed growth of 15.5% during the third quarter (after a second quarter 20% decline) and a monthly decline of 2.6% in November. Car sales recently released for full year 2020 show a 29% decline in the number of units to the lowest level since 1984. More recent survey data, up to mid-January shows poor retail sales comparisons, while the unemployment rate (3 months to November) stands at 5% and the adjusted rate of earnings growth has dropped to 2%, according to the ONS. In addition to lockdown effects, certain economic sectors have suffered from shortage of components e.g cars, shipping container log jam (especially meat, fruit, and vegetables) and Irish trade disruption, largely Brexit related. Full year 2020 GDP is estimated to be down over 10%, near the bottom of the G 20 group.

However, although the effect Covid-19 variants and the vaccine roll out may be moving targets, economic estimates and corporate confidence are starting to rise from spring/summer 2021 onwards. Forward looking economic growth estimates cover a wide range, as the positive argument of relief/catch up spending, by an element of the population from records savings (savings ratio 27.4% in Q2) has to be balanced against rising bankruptcies, short term unemployment, greater poverty, loan repayments and the spectre of higher taxes, and certain residual Brexit negatives (e.g. trade admin, tourist travel, financial services, EU defence, pharmaceutical co-operation, airline shareholder voting structure, Scottish/Irish future…)

The Chancellor’s Autumn statement, full of records of an unwelcome variety, highlighted the weak economic growth (-11.3% 2020, followed by 5.5% then 6.6%), budget deficit 19% of GDP this financial year and an expectation of 2.6 million unemployed. Various support packages have been extended to March/April. Much of the early March Budget debate is likely to centre on the extent and appropriateness of tax increases

Analyst’s estimates expect average global corporate earnings to decline around 17%in 2020 with a tentative rebound of over 25% next year Source (Morgan Stanley). There is exceptionally large country to country variation. Europe, including UK, is expected to underperform the US in 2020 while outperform in 2021, while Japan is one of the zones experiencing more economic and corporate resilience. This is also true in China, but also Korea and Taiwan where the combination of better COVID experience and export mix (technology, medical) is cushioning the economic blow. Reflecting the above and noting index sectoral breakdowns, dividends seem likely to fall furthest and recover most strongly in Europe.

At this time of writing approximately 85% of US companies have released quarterly results, with the average eps growth beating expectations significantly. Off a smaller reporting sample so far, UK and European companies are also topping estimates.

Although currently further from investor worries, growing concerns regarding global trade tensions (many), government debt (over 100% Debt/GDP), USA/China/Russia/Australia/Hong Kong, Middle East relations, BREXIT follow up and possible taper tantrums. It will be increasingly important to watch inflation trends, as any “shock†necessitating greater than forecast bond yields could have serious repercussions for many asset classes.

More intangible in nature, the pandemic also seems certain to amplify global inequalities (regional, medical, employment, poverty, demographic) which could manifest in growing social unrest.

Equities

Global Equities showed a gain, in aggregate over December 2020. The FTSE ALL World Index registered a gain of over 1.42% over the month in local currency,0.6% sterling adjusted. The UK broad and narrow market indices rose by approximately 1% during January, much in line with the world average. Emerging markets, Asia and the NASDAQ led the monthly gain, while Europe lagged. t The VIX index, ending the month at 31.9, showed a monthly gain of 40.0%, much due to speculative activity at the end of the period..

FTSE100-12-month Graph

- Foreign ExchangeThe major currency developments during the month were the strength of the UK pound and US dollar against the Japanese Yen and Euro. During the month, the Chinese Renminbi continued to strengthen and now stands at 1 USD=6.4608 Yuan. Adjusting major indices to sterling shows nearly all major indices showing a return of approx. 1% for the month of January!CommoditiesWith few exceptions, commodities rose in price terms during January. The exceptions included gold, silver, palladium, coal, and soya. Chinese demand seems likely to drive the industrial metals higher. Interestingly, near the month end, some of the “other†cyber-currencies were drawn into the retail frenzy.Looking ForwardNotwithstanding the large human toll and uncertainly still posed by Covid-19 (lockdowns, geographical variations, vaccines) there is growing optimism regarding the course of the global economy.Central banks continue to adopt an easy money policy, supplemented by other measures while Governments provide increasing short- and long-term fiscal support.However, both supports will inevitably be questioned/reversed as and when the pandemic eases, and investors will have to assess the impact on various asset classes.For equities, the two key questions will be whether/if rising interest rates eventually cause equity derating/fund flow switches, government, corporate and household problems, and how the rate of corporate earnings growth develops after the initial snapback.Following the format of last month, I make the following observations.Observations/Thoughts

- SECTORS-The dramatic change in equity confidence, from early November, largely as a result of the Biden election victory and vaccine announcements prompted large sector/style changes with new focus on value, cyclicals expected to benefit from sharper economic growth. Since the turn of the year the rally has broadened encompassing pharmaceuticals for instance, while the Saudi move in early January has invigorated the oil and gas names, the laggards of 2020.Over coming weeks corporate results, and more importantly, accompanying statements will be scrutinised for future pointers.

- There has been significant performance variation between my three bespoke stock buckets, balanced, high risk and low risk since November 6th, the weekend of the first significant vaccine announcement and the US election. As the benchmark the FTSE, S&P and NASDAQ have risen approximately 9.3%,7.5% and 12.1%respectively between close 6th November and January 28th.Over the same period, many of the “higher risk†usual suspects,IAG,Carnival,Easyjet,Cineworld and Gym Group have risen by over 35%,though still well down on 2019 high prices, and below the 50% gains I mentioned at the end of December.However,mainstream stocks in the area of oil and gas,banks,insurance,appear and property have also shown above average gains on the expectation of rising economic growth late 2021 (and higher rates/lower defaults/dividends in the case of the banks).Conversely the defensive basket has shown a negligible move, with price declines for instance in some of the pharmaceutical names.

- The last months have shown the importance of maintaining a balanced portfolio. Many companies in the value/cyclical area seem likely to recover further, while great selectivity will be required chasing the Covid-19 risk stocks. Some of these names could recover quite strongly but risks of bankruptcy, dilution, government interference/control should be considered.Conversely,previous†winners†have to be assessed both on their relative valuation, as well as relative earnings growth in a post pandemic world.

- Emerging Markets-Very difficult to adopt a “blanket†approach to the region with so many different COVID, commodity, debt, geo-political variables. Although the region is currently receiving large fund inflows, largely on aggregate valuation grounds, extra due diligence is required. Currencies played a major role in 2020 returns.

- However, I continue to have a relatively favourable view on Vietnam, where the macro factors (COVID success, economic GROWTH!), stable FX,inward investment are positive features. Other Asian markets are also worth a look e.g South Korea, Taiwan where relative pandemic experience, economic fundamentals and index/export breakdowns compare favourably. Russia, both bonds and equities, may appeal to value, income-oriented investors and enjoys a relatively favourable current/fiscal balance situation, although political developments can unsettle. The active versus passive debate in 2021, will take extra significance where “China versus the rest†and appropriate tech weighting will be important considerations.

- Not on near term investor (or government!) worry lists but be aware of the huge government DEBT problem building (tax increases sooner or later). Latest figures show aggregate global debt in excess of GDP at the global level and the mantra of extremely low servicing costs, is just that! The USA specifically is aiming to increase the percentage of longer maturity issuance in 2021. Apart from short term haven buying, I expect conventional government FIXED INTEREST to suffer in the medium term and would expect 1% to become a floor rather than ceiling for the US 10-year yield. According to Citi Private Bank strategists about 80% of investment grade debt yields less than 1%, a tough starting point. However, other fixed interest options are available after, making appropriate allowance for risk,transparency,trading, liquidity etc.

- FX-The major currencies have started 2021 in a relatively calm manner despite an abundance of geo-political, macro-economic and COVID19 news. Many bearish US Dollar calls made at the turn of the year appear to have moderated while sterling may be receiving more attention on relative vaccination news/Brexit relief, even though short-term economic prospects are dire. In the absence of another major global shock, the Japanese Yen may lose some of its haven attractions. The Chinese Renminbi continues to grind higher, something which should be factored in emerging market discussions.

- COMMODITIES- Gold has been moving sideways since August 2020, and while longer term inflationary reasons and diversification benefits may apply, the prospects for more cyclical plays may be more interesting now. Copper, which has rallied significantly about since its March low, has benefitted from Chinese demand, “green†stimulus issues and some Covid-19 related supply issues and iron ore/coal are benefitting from a steel (especially in Asia) revival. Increased renewable initiatives, greater infrastructure spending as well as general growth, especially from Asia, are likely to keep selected commodities in demand

- ESG Considerations-I have been reviewing several ESG (Environmental, Social and Governance) issues recently, both from personal interest, client curiosity and cognizant of the huge amounts of resource (both human and financial) being diverted to the sector. While applauding the longer-term merits of such a move, I would advise extra layers of due diligence regarding “greenwashingâ€, choice of benchmarks, and shorter-term considerations of values versus wallet, increasing stretch between tech and oil being a good example. A few days ago, Imperial Brands held a very encouraging capital markets day and explained their long term strategy. At the current price, they pay a very well covered, and growing dividend that puts the shares on a 9.5% annual yield.What price morals?

- Environment is expected to appear strongly on US, UK, and European political agendas over coming months. There are several infrastructure/renewable investment vehicles which currently appear attractive, in my view, combining well above average yields and low market correlation with low premium to asset value

- Speculative Activity- Several anecdotal indicators, which have appeared recently, in my universe such as volatility in the volatility index, cyber currency gyrations, rapid growth in SPAC’s, certain IPO debuts, massive option trading, meteoric rise in openings of day trading accounts and finally “the battle of Reddit versus hedgies†akaâ€main street versus Wall Street†(see below)…are flashing red indicators to me ,suggesting there will be financial casualties soon, sometimes in unpredictable areas. Many reasons have been cited for some of the retail behaviour including shortage of more “rational†investment options, more people screen watching/trading/social media/ easy finance/ fractional share trading/ commission free trading and, US specific, one off stimulus cheques. There will be large, short term winners and losers from the current situation, but many of the factors above are still present, if laws are not broken, this new force should be factored into asset price behaviour. The regulators will have to be incredibly careful in being seen not to “take sidesâ€, as will the brokers/platforms. There will continue to be high/risk/return opportunities for savvy investors. Much larger companies such as Nokia, Cineworld,Hammerson and Pearson Plc have already been caught in crossfires and there will be more.